Governed Agentic Harnesses: A Control Architecture for Agentic AI in Regulated Finance

A Financial-Industry Pattern for Safe, Auditable, and Production-Ready Agentic AI

June 2026 , Tao Jin, Pyligent AI

A practical white paper for financial institutions, fintech builders, AI platform teams, and model-governance leaders who need agentic AI to be useful without becoming uncontrolled decision infrastructure.

Executive Summary

Financial institutions are moving from chatbot pilots toward agentic AI systems that can read documents, call tools, route data, generate recommendations, and coordinate multi-step workflows. This shift creates a new engineering and governance problem. General-purpose agent frameworks are good at completing tasks, but regulated finance requires something stricter: traceability, evidence, controls, data-quality gates, human review, and clear separation between model-generated proposals and institution-approved decisions.

This white paper introduces the Governed Agentic Harness: a reusable control-plane pattern for deploying agentic AI in high-stakes financial workflows. Its core principle is simple:

Agents may propose, but gates dispose.

In this pattern, models, agents, and tools do not directly make admissible decisions. They produce typed, versioned, evidence-backed artifacts. Independent deterministic gates then decide whether those artifacts can advance, require human review, or must abstain. The result is an architecture that preserves the productivity of AI agents while meeting the risk, audit, and accountability expectations of banks.

Pyligent AI has instantiated this pattern in CSA-aware collateral management, where raw ISDA Credit Support Annexes (CSAs), margin data, inventory, CRIF/SIMM-style traces, and current allocations are transformed into source-faithful, optimization-ready collateral data models. The same pattern generalizes to other financial workflows including KYC/AML, credit review, loan-document processing, treasury operations, regulatory reporting, insurance underwriting, and model-risk documentation.

Why Agentic AI Needs a Financial Control Plane

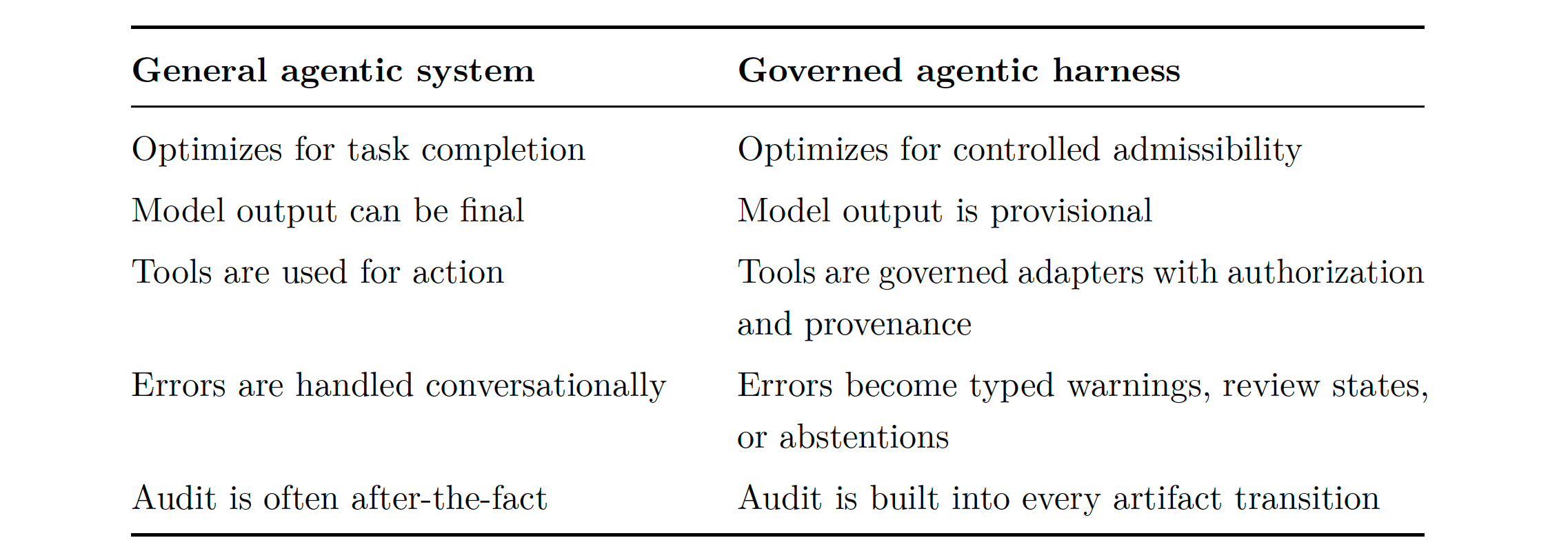

Most agentic AI frameworks are optimized for action: reason, call tools, retrieve information, and produce a result. That is useful, but insufficient for regulated finance. In banking, a result is not valuable simply because it is plausible or fast. It must be admissible.

A finance-grade AI workflow must answer questions such as:

What source document or system produced this term?

Which model or rule extracted it, and under which prompt or version?

Does the evidence actually support the extracted value?

Is the output schema-valid and complete enough for downstream use?

Are unresolved legal, rating, or operational terms review-gated?

Can the recommendation be certified against domain constraints?

Who can approve, override, or escalate the result?

Traditional model-risk frameworks were largely designed around static or bounded models. Agentic systems are different: they maintain state, call tools, invoke external systems, and generate intermediate artifacts. This means banks need a control plane around agents, not only better prompts or larger models.

The Governed Agentic Harness fills that gap. It turns agentic AI from an open-ended task runner into a controlled workflow system with typed artifacts, deterministic gates, tool boundaries, audit trails, and human-review states.

The Governed Agentic Harness Pattern

A Governed Agentic Harness is an architecture that places agents inside a controlled execution envelope. The harness defines what agents may observe, what tools they may call, what artifacts they may create, what evidence they must attach, and which deterministic gates decide whether outputs can be used.

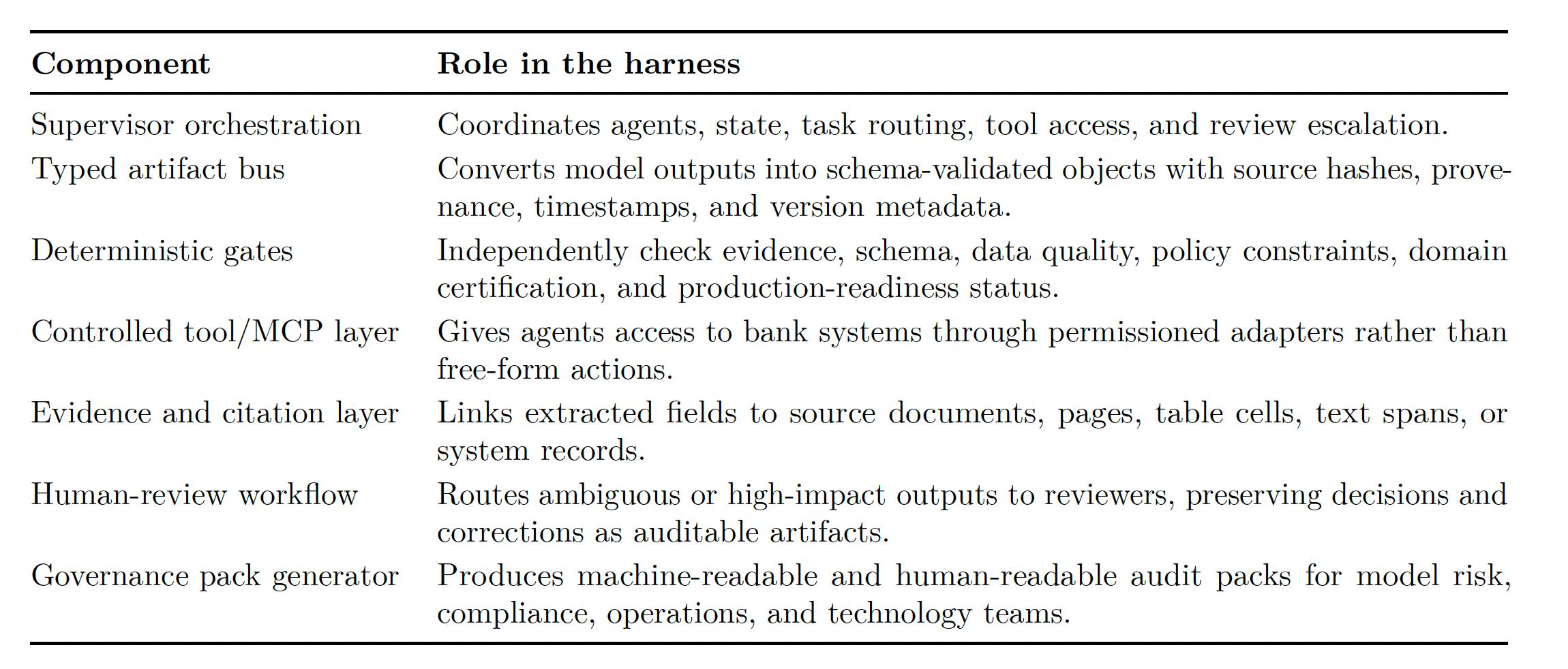

Core Design Components

From Agent Framework to Admissibility Framework

The key innovation is not simply adding more agents. It is changing the unit of control. In many agentic systems, the model response or tool result is the final product. In a governed harness, the final product is an admissible artifact: a structured object that has passed independent checks and can be inspected, replayed, or rejected.

This pattern is especially important in finance because the cost of a wrong answer is not only user dissatisfaction. It can be a failed control, an incorrect regulatory report, an invalid collateral call, a misclassified client, or an unsupported credit decision.

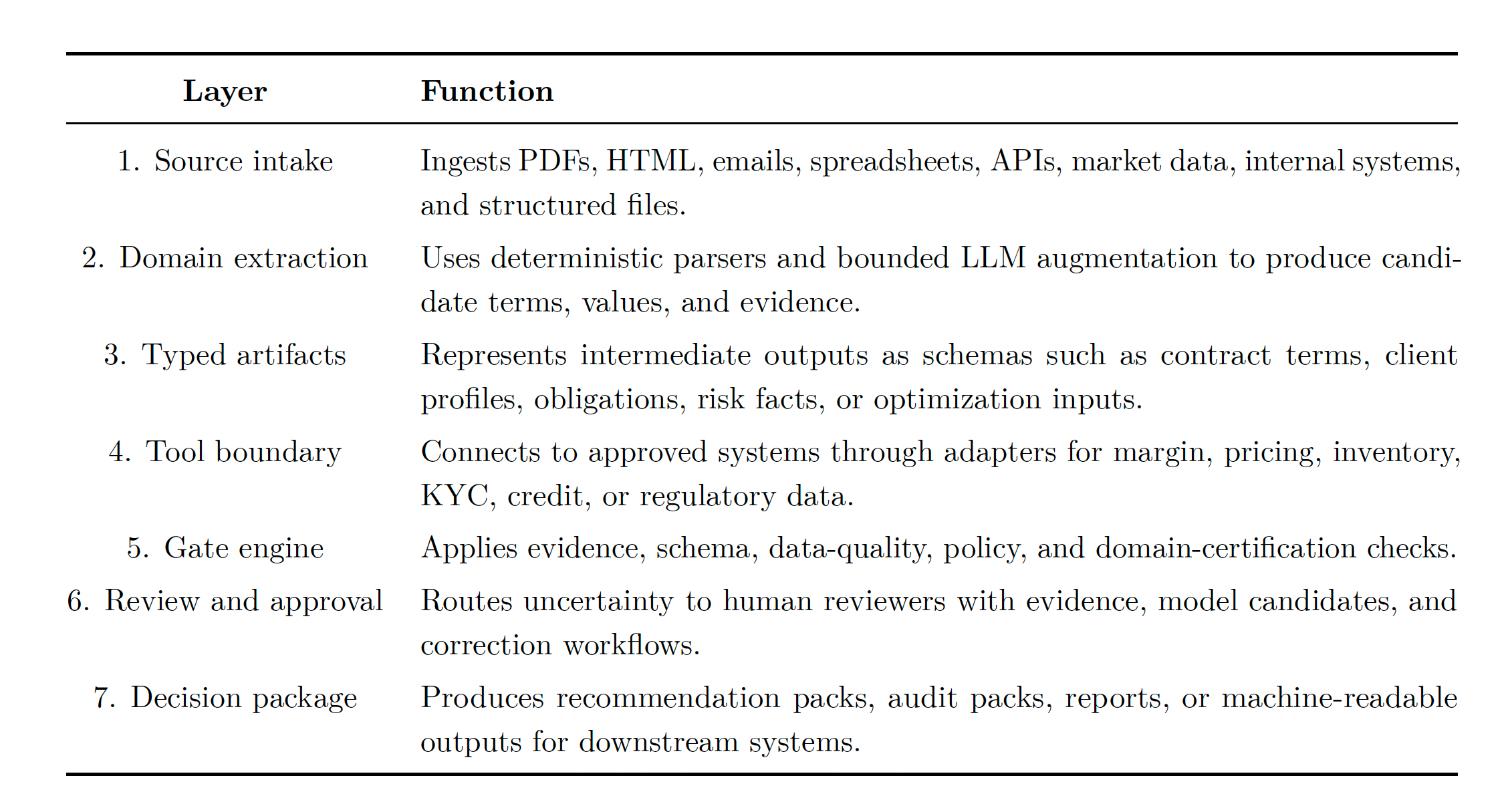

Reference Architecture for Financial Workflows

The Governed Agentic Harness can be viewed as a layered architecture:

The same architecture can support many financial use cases. The domain schemas and gates change, but the pattern remains stable.

Flagship Use Case: CSA-Aware Collateral Management

Collateral management is a strong test case because it combines legal-document intelligence, numerical optimization, market constraints, operational controls, and audit requirements. A collateral recommendation may depend on:

Legal terms from ISDA CSAs, including MTA, thresholds, rounding, eligible collateral, rating triggers, and valuation percentages.

Margin requirements, including VM, IM, independent amount, CRIF traces, or SIMM-style calculations.

Inventory availability, haircut rules, concentration limits, settlement constraints, and custody policies.

Certification checks such as zero-shortfall, eligibility, valuation policy, and review-required states.

Pyligent’s implementation follows a deterministic-first and evidence-gated approach. Raw CSA sources are parsed from HTML and PDF, including complex collateral schedules and haircut matrices. LLM augmentation is used only as a bounded semantic repair layer. It may help map asset descriptions, maturity buckets, or ambiguous clause structure, but it cannot invent values, numeric valuations, or production decisions. Every matrix row and normalized rule must remain source-linked and review-gated when unresolved.

CSA-to-Decision Workflow

Document ingestion: CSA documents arrive as SEC HTML exhibits, native PDFs, or scanned/partially structured PDFs.

Core term extraction: The harness extracts parties, base currency, eligible currencies, MTA, rounding, IA/IM/SIMM flags, governing law, and substitution terms.

Collateral schedule recovery: HTML DOM parsers, PDF layout extraction, Docling table artifacts, prose recovery, and bounded semantic repair recover eligible collateral lists and haircut matrices.

Matrix normalization: Source-backed collateral rows become normalized optimizer rules only when asset type, maturity bucket, rating event, valuation percentage, and evidence are valid.

Tool integration: Margin, CRIF traces, inventory, current allocation, and market-data adapters provide controlled inputs.

Certification: Candidate allocations must pass deterministic gates such as eligibility, valuation policy, zero-shortfall, and governance checks.

Audit package: The final package includes source evidence, model artifacts, warnings, review states, and production-readiness labels.

This workflow illustrates the broader innovation: the AI system is not simply extracting text or solving an optimization problem. It is building a governed decision chain from unstructured financial documents to auditable, typed artifacts.

Optimization Workflow Summary

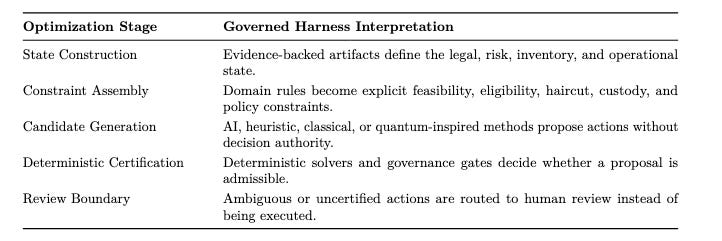

Many high-value financial workflows are not pure document-understanding tasks. They are governed optimization workflows: an institution must transform legal terms, risk facts, inventory, market data, and policy constraints into a recommended action that is both economically useful and control-admissible. The harness pattern supports this by separating the optimization lifecycle into explicit stages:

Source-to-state construction: extract contract terms, portfolio facts, inventory, limits, and risk measures into typed artifacts with evidence and provenance.

Constraint assembly: convert legal, operational, liquidity, concentration, settlement, and custody rules into machine-checkable constraints.

Candidate generation: use classical heuristics, mathematical programming, AI planners, or quantum/quantum-inspired candidate generators to propose feasible or repairable actions.

Deterministic certification: certify every candidate against hard constraints, objective definitions, evidence requirements, and governance rules.

Review and execution boundary: route uncertified or ambiguous candidates to human review and expose only certified, policy-approved recommendations to downstream systems.

In collateral management, this flow turns CSA terms, margin requirements, CRIF/SIMM-style traces, current allocation, and inventory into certified collateral recommendations. The same workflow shape applies to portfolio rebalancing, liquidity allocation, treasury funding, trade exception resolution, credit covenant actions, and insurance portfolio optimization. A recent companion paper, A Certified Higher-Order Quantum Framework for CSA and Margin-Aware Collateral Optimization, develops the optimization side of this workflow in more detail, showing how higher-order candidate generation can remain bounded by deterministic CP-SAT certification and margin-source provenance.

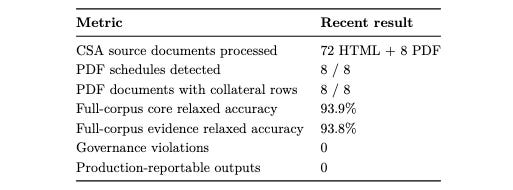

Benchmark and Evaluation Evidence

Pyligent’s CSA implementation has been evaluated across HTML and PDF CSA sources, with downstream optimization and governance checks. A related research paper, Hybrid LLM and Higher-Order Quantum Approximate Optimization for CSA Collateral Management, describes an earlier technical pipeline for evidence-gated CSA extraction and certifiable collateral optimization. A newer companion manuscript, A Certified Higher-Order Quantum Framework for CSA and Margin-Aware Collateral Optimization, further formalizes the optimization layer as a certified, adapter-first collateral allocation framework in which margin requirements are normalized upstream and candidate allocations are certified before reporting.

Recent evaluation runs demonstrate both capability and control:

In the real Bank PDF regression case, the system reconstructed 43 out of 43 expected haircut-matrix rows, preserved all non-numeric “To be agreed” cells as review-required, introduced no unsupported numeric values, and produced no certification-eligible unresolved rows. This is a useful example of the harness principle: more extraction coverage is valuable only when paired with evidence, abstention, and certification controls.

The benchmark does not claim that every output is production-ready. Instead, it demonstrates a safer operating model: high-confidence extracted terms can flow forward, while unresolved collateral rows, ambiguous valuations, local rating-scale issues, and incomplete schedules are review-gated or blocked.

Innovation: A Reusable Pattern for Finance and Fintech

The Governed Agentic Harness has implications beyond collateral management. It introduces a practical pattern for how fintech platforms, bank AI teams, and enterprise software providers can safely productize agentic AI.

Technical Differentiators

Artifact-first AI: The core object is not a chat response while a versioned artifact with schema, evidence, provenance, and status.

Decision authority separation: Models propose values; deterministic gates decide admissibility.

Adapter-first integration: External systems are reached through governed APIs, MCP-compatible tools, or controlled adapters.

Evidence as infrastructure: Citations, page spans, table cells, and source hashes are first-class data, not optional explanations.

Review-aware automation: The system can abstain, warn, or route to human review instead of forcing an answer.

Domain-certified outputs: Results must satisfy financial constraints such as zero shortfall, eligibility, data-quality status, and valuation policy.

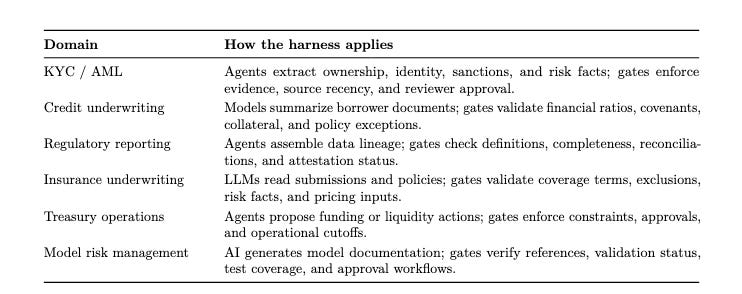

Reusable Financial-Industry Applications

This generalization is important for the fintech ecosystem. Many AI products today are either vertical point solutions or generic agent frameworks. The Governed Agentic Harness sits between them: a reusable financial AI control plane that can be specialized by domain artifacts, policies, and tools.

Deployment Model for Banks

A governed harness can be deployed incrementally. Banks do not need to automate final decisions on day one. A practical adoption path is:

Review-assisted extraction: Use the harness to generate evidence-backed artifacts and reviewer queues.

Controlled decision support: Allow certified artifacts to feed recommendations while unresolved terms remain blocked.

Policy-governed production: Enable production use only for source-supported, schema-valid, certified, and monitored workflows.

Closed-loop improvement: Use reviewer corrections, failed gates, and gold-label audits to improve deterministic rules, prompts, taxonomies, and parsers.

This path aligns AI adoption with existing governance functions. Legal, operations, risk, compliance, technology, and model-risk teams can all inspect the same artifacts rather than relying on opaque model behavior.

Conclusion

Agentic AI will become part of financial infrastructure. The question is not whether banks will use agents, but whether those agents will be governed well enough to operate in high-stakes workflows.

Pyligent’s Governed Agentic Harness offers a practical answer. It preserves the advantages of AI agents — language understanding, tool use, semantic repair, and workflow coordination — while adding the control layers finance requires: typed artifacts, evidence, deterministic gates, controlled tools, human review, and audit packs.

Collateral management is the flagship example, but the broader message is larger. The fintech industry does not only need more capable agents. It needs a new category of infrastructure: governed agentic control planes that make AI outputs admissible, auditable, and usable inside regulated institutions.

About Pyligent AI

Pyligent AI builds the governance layer that enables banks and fintech platforms to safely deploy agentic AI in high-stakes financial workflows. Its Governed Agentic Harness pattern is currently instantiated in CSA-aware collateral management and is designed to generalize across financial document, risk, compliance, and operational decision workflows.

Request a Demo or Engage in Technical Discussions

Pyligent AI welcomes conversations with banks, fintech platforms, risk teams, legal operations groups, collateral desks, and technology partners interested in governed agentic AI. To request a product demo, discuss a pilot workflow, or explore research and implementation collaboration, please contact us below.

Contact

Tao Jin, Founder & CEO

Email: tao.jin@pyligentai.com

Website: https://www.pyligent.com

|

References

[1] T. Jin, S. Florescu, and H. Jin, “Hybrid LLM and Higher-Order Quantum Approximate Optimization for CSA Collateral Management,” arXiv:2510.26217, 2025. Available: https://arxiv.org/abs/2510.26217.

[2] T. Jin and S. Florescu, “A Certified Higher-Order Quantum Framework for CSA and Margin-Aware Collateral Optimization,” arXiv:2606.04235, 2026. Available: https://arxiv.org/abs/2606.04235.